Beef Market Trends

With continued international uncertainty, an improvement in domestic seasonal conditions, and new price records, it has been a dynamic time in the beef market to say the least.

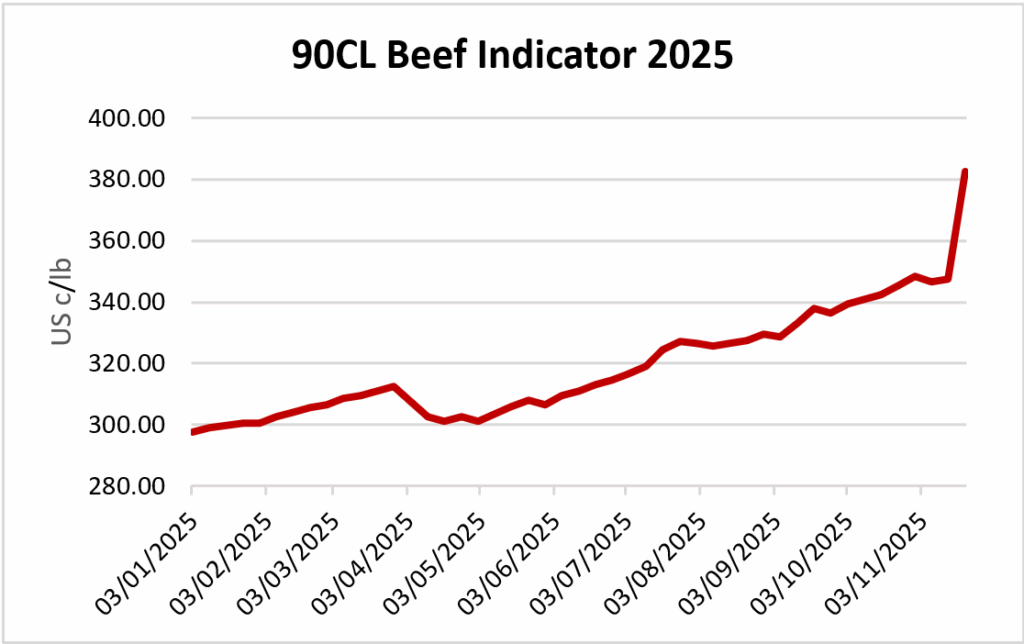

90CL Records

Much like a kangaroo on a trampoline, the 90CL price indicator has reached new heights in 2025, breaking and re-breaking record prices. 90CL stands for 90% Chemical Lean and is the main beef price used as an indicator of beef entering the US. This indicator has peaked near 300 US c/lb in 2014, 2019 and 2022, however this year it has left those peaks in the dust, exceeding 380 c/lb.

Tariff Rollercoaster

The word tariff has found its way into the vocabulary of many around the world since US reciprocal tariffs were imposed in early April.

Australia was comparatively well off, facing one of the smallest tariff levels at just 10% while our main competitor in the US beef import market, Brazil, at the peak experienced a total tariff rate of 76.4%. Before the implementation of this restrictive rate Brazil had more than doubled their import volume year on year however the revised tariff level rendered Brazilian beef all but economically unviable in the US market.

Fast forward to November and hundreds of these reciprocal tariffs were removed, including most tariffs on beef imports such as the 10% faced by Australian beef. Theoretically this should make imported beef cheaper for US consumers however with the tight domestic availability and imports already trading at a discount to domestic product this margin will probably be used to secure beef imports at higher prices. With Brazil returning to their out of quota tariff rate of 26.4%, larger volumes of Brazilian imports are expected which will limit the potential increases to imported Australian beef prices.

Rebuild!

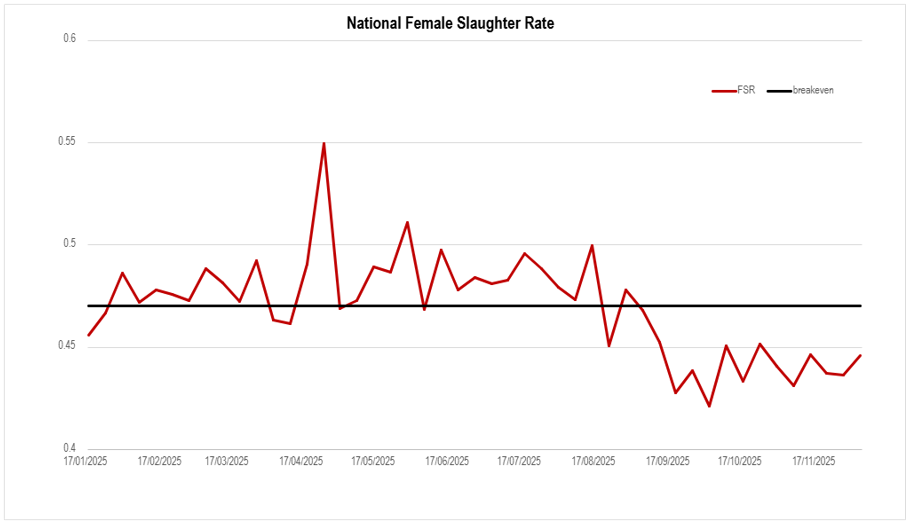

The position of Australia’s domestic herd has been rather friendly with the breakeven level of female cattle slaughter for most of 2025. It is widely considered that a female slaughter rate (FSR) of 47% is the breakeven level at which the domestic herd is neither growing nor shrinking and in early September, after months of hovering just above this level, the Australian herd entered a rebuild phase.

This reduces the supply of beef as producers hold on to more female animals as breeders and will ultimately put upward pressure on cattle prices.

With robust demand for, and constricting supply of Australian beef, the short-term outlook for the industry is positive. As commercial beef producers start to experience higher prices for their product, demand will increase for quality genetics, one of their inputs, which will increase prices for registered Angus bulls. Amid much uncertainty, 2026 is looking favourable for both commercial and seedstock producers in the Australian cattle industry.

Until next time,

Harry Lynn – Economic Research Assistant to CEO

Disclaimer: This market report is ultimately the view of the author and does not constitute professional advice for business decisions.